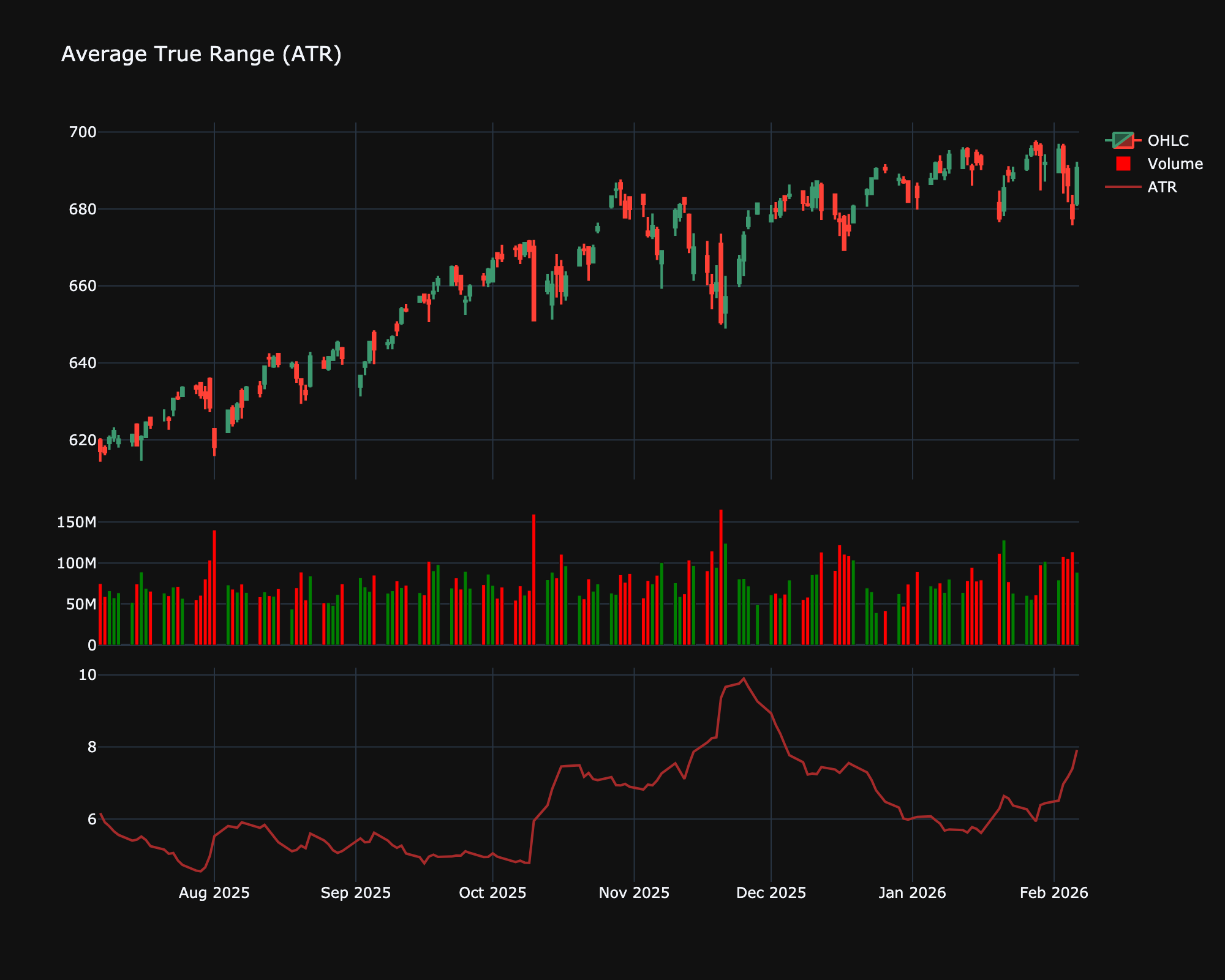

Average True Range (ATR)¶

| Name | Type | Prerequisite | Use Cases |

|---|---|---|---|

| Average True Range (ATR) | Volatility | EMA | Setting volatility-based stop losses. |

Definition¶

The Average True Range (ATR) is a technical analysis indicator that measures market volatility. It is typically derived from the 14-day simple moving average of a series of true range indicators.

Mathematical Equation¶

\[

\begin{align}

TR &= \max[(H - L), |H - C_{prev}|, |L - C_{prev}|] \\

ATR &= \text{SMA}(TR, n)

\end{align}

\]

Special cases¶

- Maximum possible value: Unbounded

- Minimum possible value: 0

- Behavior: Moves independently as an absolute value measuring market volatility, regardless of trend direction.

Visualization¶

Trading Significance¶

-

Volatility Measurement: High ATR = High Volatility. Low ATR = Ranges.

-

Stop Loss: A multiple of ATR is often used to set stop-loss levels (e.g., 2x ATR).