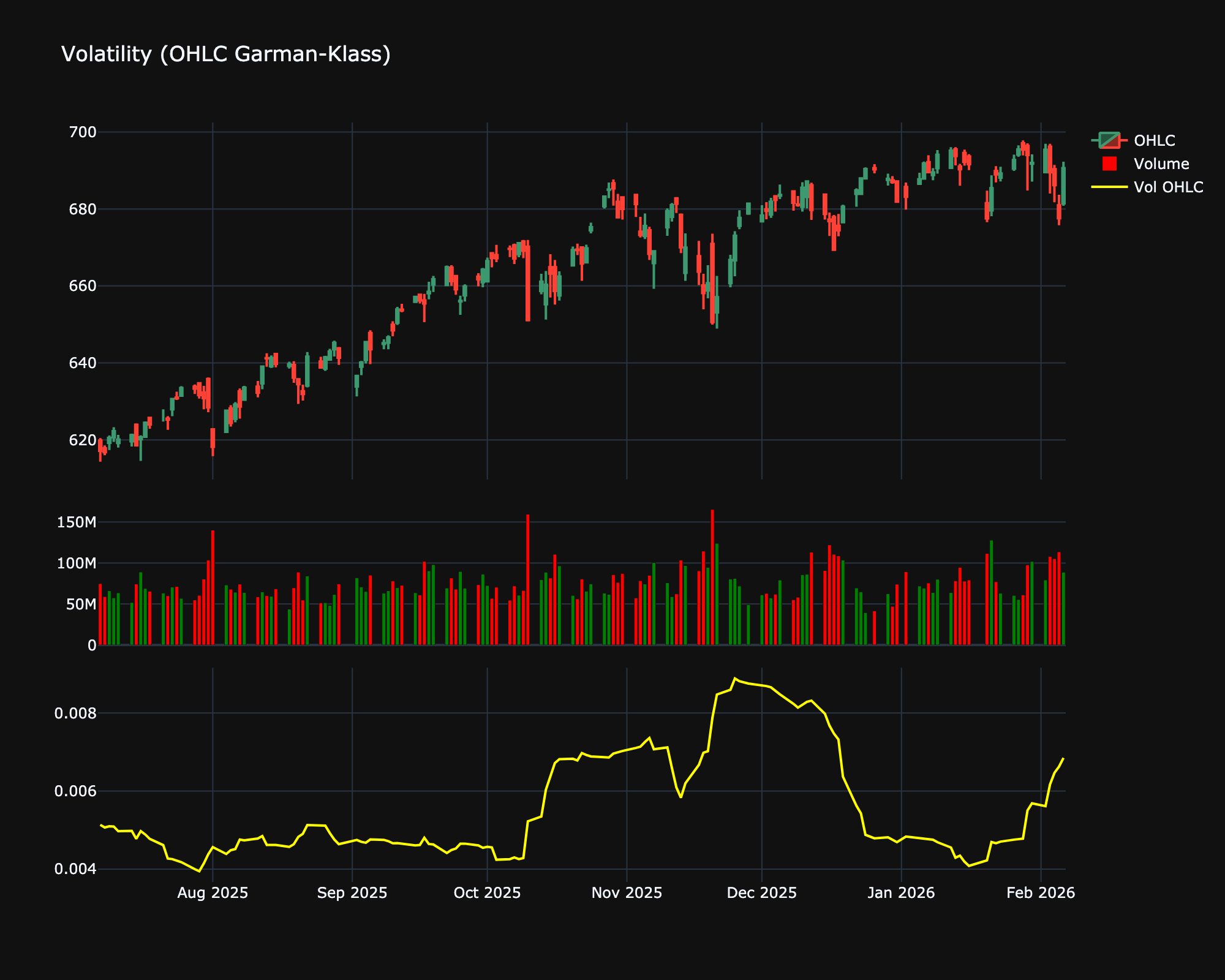

Volatility (OHLC Garman-Klass)¶

| Name | Type | Prerequisite | Use Cases |

|---|---|---|---|

| Volatility O-H-L-C (OHLC Vol) | Volatility | OHLC Data | Provides a more granular risk assessment than close-only models. |

Definition¶

The Garman-Klass volatility estimator is an extension of the Parkinson estimator that includes opening and closing prices, not just High and Low. It is more efficient than Close-to-Close volatility as it utilizes information from the entire bar.

Mathematical Equation¶

\[

\sigma^2 = 0.5 \ln\left(\frac{High}{Low}\right)^2 - (2\ln 2 - 1) \ln\left(\frac{Close}{Open}\right)^2

\]

Special cases¶

- Maximum possible value: Unbounded

- Minimum possible value: 0

- Behavior: Moves independently to represent price variance integrating OHLC data.

Visualization¶

Trading Significance¶

-

Efficiency: Provides a more accurate estimate of volatility by incorporating intraday range and opening gaps.

-

Intraday Risk: Better captures the true trading range risk experienced during the session.