Standard Deviation¶

| Name | Type | Prerequisite | Use Cases |

|---|---|---|---|

| Standard Deviation (StdDev) | Volatility | OHLC Data | Quantifies market risk and serves as the backbone for Bollinger Bands. |

Definition¶

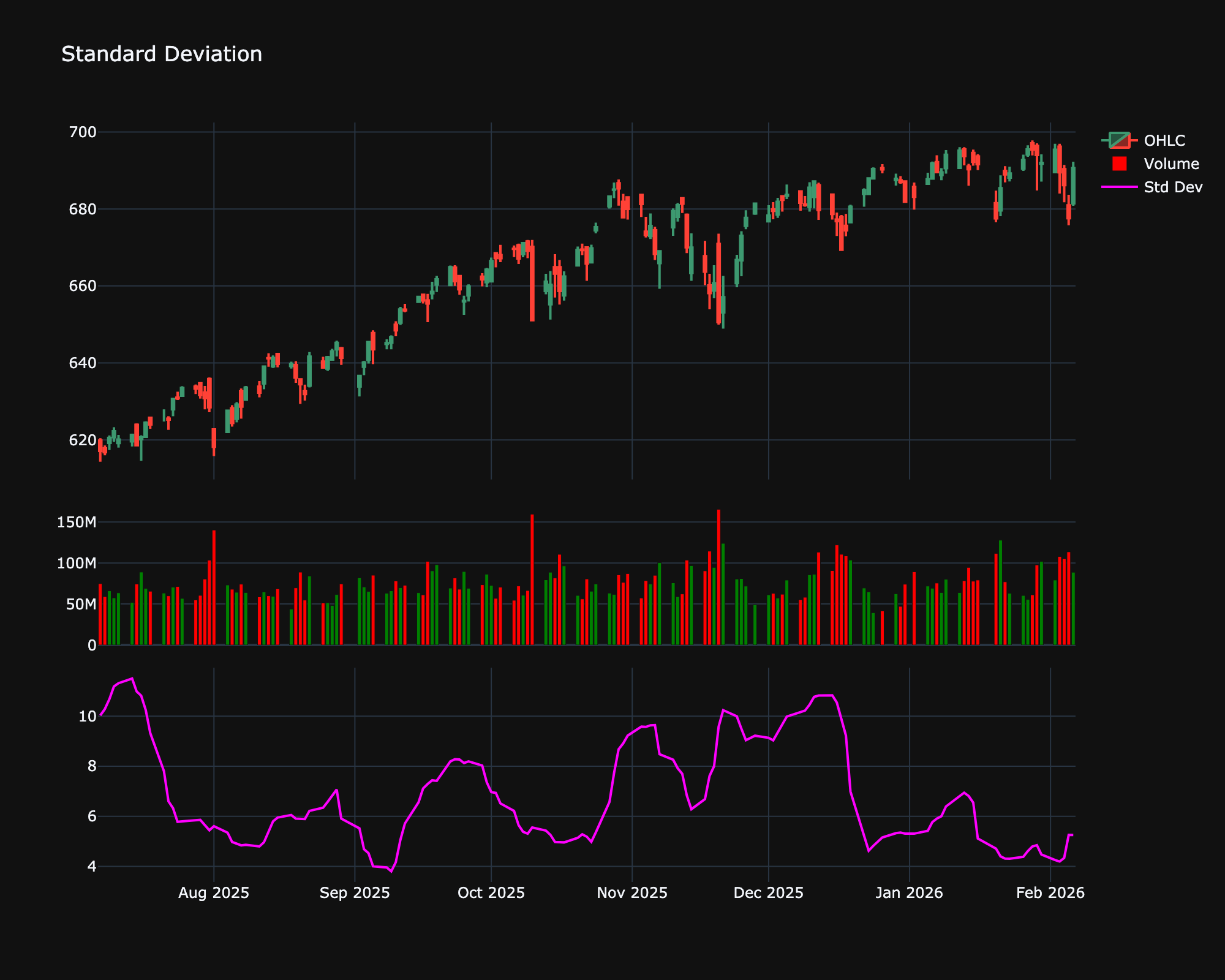

Standard Deviation is a statistical measure of volatility. In finance, it represents the dispersion of returns from the average return.

Mathematical Equation¶

\[

\sigma = \sqrt{\frac{\sum(x - \bar{x})^2}{n}}

\]

Special cases¶

- Maximum possible value: Unbounded

- Minimum possible value: 0

- Behavior: Moves independently to represent the statistical dispersion of price from its average.

Visualization¶

Trading Significance¶

-

Volatility: High Std Dev implies high volatility and potential risk.

-

Market Tops/Bottoms: Extremely high volatility often marks tops/bottoms.